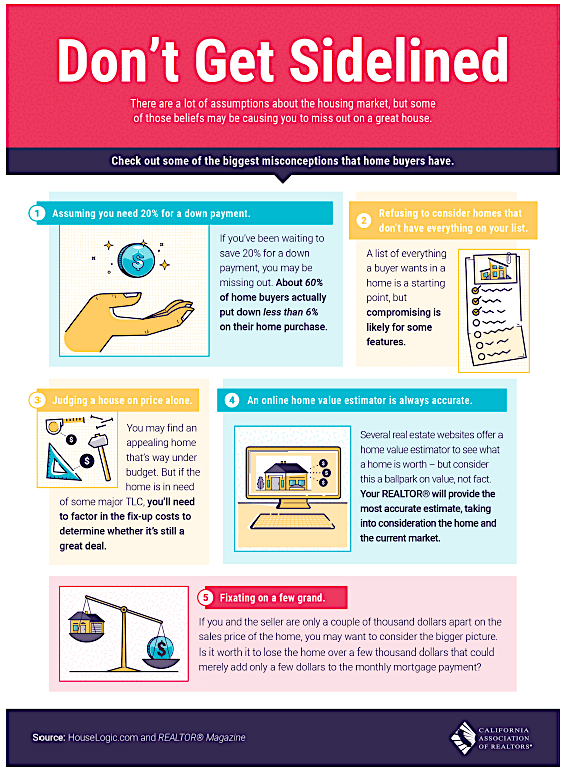

You came really close to buying that house. It had everything . . . except . . . RIGHT?! Has this happened to you? Everything about that home tour was going great until the agent said “oh don’t forget there’s no AC in this home,” and instantly you were turned off and heading straight for the door! Although central air and air conditioning has become hugely popular amongst home buyers in almost region of the county, you found yourself looking at a home that was missing that one “thing” which killed your deal. Leaving you sidelined again. This months infographic was excellent because as some seasoned homebuyers know, December can be one of the best months of the year to strike a deal. There are a variety of reasons the “December Effect” exists. The bottom line is that motivations to close a deal before year end the December 31st has caused more home buyers to find a deal in the slow, dark days of winter more than any month of the year. Buying or selling, December is NOT the month to get sidelined! As the graphic shows in Box 1, over 60% of home buyers put less than 6% down to close! That reason alone can get any homebuyer off the couch and into this weekends next Open House. Box 3 gives another example of judging a home just by it’s price alone. Because of the “December Effect,” I always recommend homebuyers look at prospective homes regardless of listing price. I know of a seller in Los Angeles that listed a home for more than $2 million as a For Sale by Owner that was offered cash of $900k and a very quick closing. Instead of the seller being insulted or turning away they started negotiating the deal into the low $1 million range with the buyer. Although the deal didn’t go through for other reasons, the point is most buyers would never think that such a low offer would even be considered. And maybe that is true much of the time. But this buyer learned by writing and submitting an offer the sellers motivation was substantial enough to negotiate the deal rather than turn away. Don’t get sidelined this December! The best home buying opportunity of your life could be one Open House away!